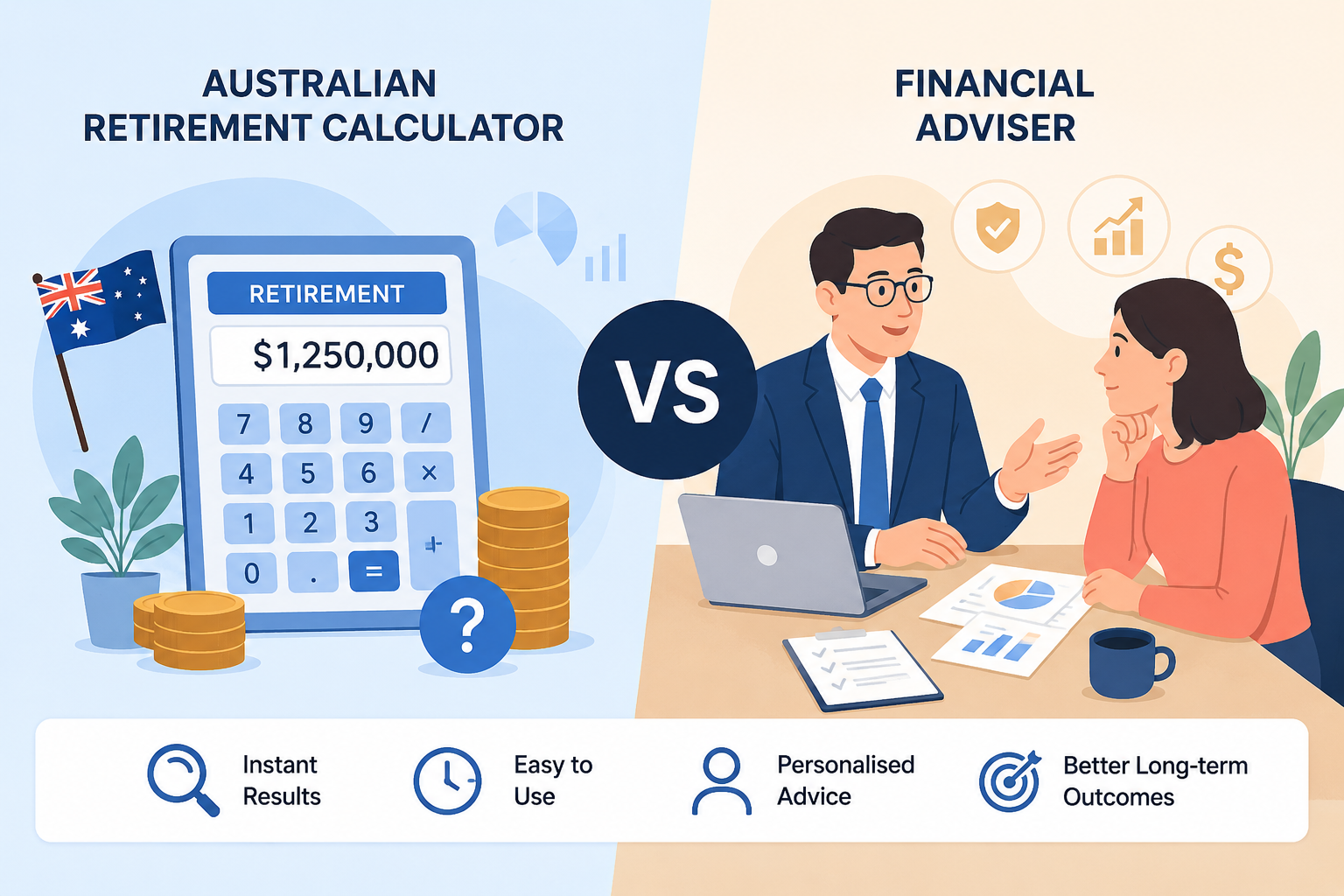

Retirement Calculator vs Financial Adviser: What’s Better?

An Australian retirement calculator is one of the most accessible financial tools available today. Free, instant, and available on dozens of websites from ASIC's MoneySmart to your super fund's member portal.

On the other hand, a financial adviser costs money, requires appointments, and involves sharing your full financial picture with another person.

So which one do you actually need?

The honest answer is that it depends on where you are in your retirement planning journey. For some Australians, a well-built calculator is genuinely enough to get clarity and move forward. For others, professional advice is the only way to get the strategy right. And for many, the best approach is both, used at the right stages and for the right purposes.

This article breaks down what each option does well, where each one falls short, and how to decide which is right for your situation.

Disclaimer: The information in this article is general in nature and does not constitute financial advice. It has been prepared without taking into account your personal objectives, financial situation or needs. Before acting on any information here, consider whether it is appropriate for your circumstances and seek advice from a licensed financial adviser. All figures and thresholds mentioned are subject to change, always verify current rates directly with the ATO, Services Australia, or ASIC's MoneySmart.

TL;DR

- An Australian retirement calculator gives you a projection based on your inputs and assumed conditions. It is a starting point, not a plan.

- A financial adviser gives you personalised, legally accountable advice built around your complete financial picture.

- ASIC research found that around half of Australians approaching retirement worry they could run out of money, yet only 26% demonstrate a strong understanding of retirement finances.

- Digital advice tools serve as a lower-cost entry point that builds toward full personal advice, with 56% of Australians with an ongoing adviser relationship seeing digital tools as valuable alongside human advice.

- Delphi IQ sits between the two, more sophisticated than a basic calculator, built on actuarial modelling, and free. It helps you get clear on your numbers before deciding whether professional advice is the next step.

What an Australian Retirement Calculator Actually Does

At its core, an Australian retirement calculator takes a set of inputs, your current super balance, income, contribution rate, age, and planned retirement date, and projects what your super might look like at retirement and how long it might last.

The better ones, like the ASIC MoneySmart Retirement Planner, also factor in the Age Pension, which makes a meaningful difference to the projected income picture. Most super fund calculators skip the Age Pension entirely, which gives you only half the picture.

A pension calculator in Australia works on the same principle, it estimates your likely Age Pension entitlement based on your assets and income, using the current Centrelink income and assets test thresholds.*

*Age Pension rates and thresholds are updated regularly by Services Australia. Always check current figures at servicesaustralia.gov.au.

What calculators do well:

- Give you a rough sense of whether you're on track

- Show the impact of different decisions, contributing more, retiring later, changing investment options

- Make retirement planning accessible without needing to book an appointment or spend money

- Help you build the financial literacy to have a better conversation with an adviser if you need one

What they don't do:

- Account for your complete financial situation, other assets, debts, a partner's income and super, property, inheritance

- Provide legally accountable advice

- Model the interaction between tax, super, the Age Pension, and estate planning simultaneously

- Give you a range of probabilistic outcomes, most calculators show one projected number, not a distribution of likely results

What a Financial Adviser Actually Does

A financial adviser can help you make financial decisions and plan for the future, including advice about budgeting, investing, super, retirement planning, estate planning, insurance and taxation. Personal financial advice is tailored to your financial situation and goals and is in your best interests.

Unlike a calculator, an adviser works from your complete picture, your super, your partner's super, your investment property, your debt, your tax position, your estate planning intentions, and your specific retirement goals. They also carry a legal obligation to act in your best interests, which no calculator can replicate.

A qualified financial adviser in Australia must hold an Australian Financial Services Licence (AFSL) or operate as an authorised representative of an AFSL holder. You can verify any adviser on ASIC's Financial Advisers Register.

What a financial adviser does well:

- Builds a strategy around your actual situation, not averages

- Identifies opportunities you may not have considered, salary sacrifice timing, downsizer contributions, carry-forward contributions, TTR strategies

- Helps you optimise Age Pension entitlement through asset and income structuring

- Provides legally accountable advice with recourse if things go wrong

- Reviews and updates your plan as legislation, markets, and your life change

Where advisers fall short for some Australians:

- Cost. Comprehensive financial advice can run to $3,000–$5,000 or more for an initial plan, with ongoing fees on top. With the cost of full financial advice remaining high under current regulatory settings, digital tools are playing an increasingly important role in bridging the advice gap.

- Availability. At the end of September 2025, ASIC reported that almost 3,500 financial advisers had not yet completed the qualifications necessary to continue providing advice to clients in 2026, contributing to a shrinking pool of accessible advisers.

- Not all advisers specialise in retirement. A generalist adviser may lack the depth needed for retirement-specific strategies like super drawdown sequencing or Centrelink optimisation.

When to Use a Calculator and When to Use an Adviser

The right answer isn't a calculator OR adviser, it's knowing when each one is appropriate.

A calculator is the right starting point when:

- You're in your 30s or 40s and want to understand broadly whether your super is growing at the right pace

- You want to see the impact of increasing contributions or changing your retirement age before making a decision

- You're trying to build enough financial literacy to have a more informed conversation with an adviser

- Your situation is relatively straightforward employed, one super fund, no major assets outside super

Professional advice is worth getting when:

- You're within 10 years of retirement and the decisions you make now have limited margin for error

- You have an SMSF or significant assets outside super

- You need to optimise Age Pension entitlement through asset structuring

- Your situation involves complex tax considerations, estate planning, or business assets

- You've used a calculator and found a significant shortfall that you're not sure how to address

- You want someone legally accountable for the advice you act on.

What Are the Best Retirement Calculator Options Available Free?

If you're starting with a calculator, the most important thing is finding one that goes beyond a single projected number and actually accounts for the variables that shape real retirement outcomes.

Most free super fund calculators use generic fee assumptions, leave out the Age Pension entirely, and produce one optimistic number based on a flat return assumption. That's a limited picture.

Delphi IQ is built differently. Rather than applying a single assumed return rate to produce one projected outcome, it uses an actuarial cashflow engine that models real-world retirement risks together, sequencing risk, longevity, inflation, and investment volatility. It factors in the Age Pension automatically and lets you compare scenarios side by side.

It's completely free and built specifically around Australia's superannuation system — the SG rate, contribution caps, concessional and non-concessional rules, and the Age Pension income and assets tests.

For anyone looking for the best retirement calculator in Australia that goes beyond a basic projection, Delphi IQ is the starting point worth trying.

Try Delphi IQ for Free

The Bottom Line

An Australian retirement calculator and a financial adviser serve different purposes. For most Australians, both have a role to play at different stages of the planning journey.

A calculator gives you accessibility, speed, and a starting point. A financial adviser gives you personalised strategy, legal accountability, and the depth to handle complexity. The gap between the two is where most Australians currently sit, and it's the gap that tools like Delphi IQ are built to help close.

FAQs

What is an Australian retirement calculator and how does it work?

An Australian retirement calculator is a tool that projects your super balance and retirement income based on inputs like your current balance, contribution rate, income, age, and retirement target. It applies assumptions about investment returns, inflation, and sometimes the Age Pension to estimate whether you're on track. The quality of the output depends entirely on the quality of the assumptions behind it. More sophisticated tools like Delphi IQ use actuarial modelling to produce a range of scenario-based outcomes rather than a single projected number.

What is the best retirement calculator in Australia?

The MoneySmart Retirement Planner, run by ASIC, is the most independent and broadly useful option. It combines super projections with Age Pension estimates and is not tied to any product or fund. For more sophisticated modelling including sequencing risk, longevity, and scenario comparisons, Delphi IQ goes further than any basic free calculator and is also free.

How does a pension calculator in Australia work?

An Australian pension calculator estimates your likely Age Pension entitlement based on your assets and income, using the current Centrelink income and assets test thresholds. It tells you whether you're likely to receive the full pension, a partial pension, or no pension based on your circumstances. Age Pension rates and thresholds are updated regularly and always verify current figures at servicesaustralia.gov.au.*

*Figures are subject to change. This is general information only.

Can a retirement calculator replace a financial adviser?

No. A calculator can give you a useful projection and help you understand the impact of different decisions, but it cannot provide personalised, legally accountable advice. It can't account for your complete financial picture tax, estate planning, SMSF, business assets, or the interaction between all of these. Personal financial advice is tailored to your financial situation and goals and is in your best interests in a way that a calculator cannot replicate.

When should I see a financial adviser instead of using a calculator?

When you're within 10 years of retirement, when your situation involves significant assets outside super, an SMSF, complex tax considerations, or estate planning, or when you've identified a significant shortfall and need a strategy to address it. A calculator is a useful starting point. A financial adviser is the right tool when the decisions you're making carry real consequences and limited margin for error.

How do I find a licensed financial adviser in Australia?

You can search by postcode on ASIC's Financial Advisers Register to find a licensed adviser near you. Look for FAAA membership and ideally a Certified Financial Planner (CFP) designation. Ask upfront how they charge, fee-for-service advisers are generally more transparent than those earning commissions. Many super funds also offer member advice services at no additional cost, which is a practical starting point.

How accurate are Australian retirement calculators?

They are useful as directional tools but not reliable as precise forecasts. Every calculator relies on assumptions about future returns, inflation, fees, and personal circumstances — none of which are knowable in advance. ASIC's research found that only 26% of pre-retirees demonstrate a strong understanding of retirement finances, which means most people aren't in a position to critically evaluate what their calculator is assuming. Always check what return rate is being used, whether results are in today's dollars, and whether the Age Pension is included.