Debt Recycling Australia: When does it work?

Debt Recycling Australia: When does it work

With the federal budget shaking up Australia's tax system, debt recycling is the strategy on the lips of every financial adviser right now. And as a nerd - I wanted to see whether it was worth it.

Most articles lead with the tax benefits top of mind. They illustrate the benefits and savings in interest deductions - with the whole purpose of the strategy is to save on tax (which in some cases it can be).

But when assessing a strategy - one should look at all the components. Tax benefits being one of them. The primary question is the one that determines whether this strategy builds wealth or destroys it; is much simpler:

Are your investment returns higher than your interest rate?

If yes, debt recycling works. If not, the tax benefits don't save you.

That's the whole argument. Almost everything else should be left in the fine print.

Disclaimer: This article is opinion based and contains general information only and does not constitute financial or tax advice. Debt recycling involves significant financial risk including potential loss of capital. Before implementing this strategy, seek advice from a licensed financial adviser and registered tax agent.

TL;DR

- Debt recycling is simple: use your existing home loan to borrow money and invest in stocks.

- It only works reliably when stock returns exceed your interest rate. When they don't, it destroys wealth.

- The RBA cash rate is currently 4.35%. Source: RBA. Variable home loan rates are running higher than this.

- The long-term average annual return for Australian shares is approximately 8% per year including dividends. Source: RBA Research Discussion Paper 2019-04.

- The tax deduction on investment loan interest is real and confirmed by the ATO; but it doesn't make a losing investment profitable.

- This is a 10–20 year strategy. It is not for everyone.

What Is Debt Recycling, Actually?

The concept is straightforward. Your home loan already exists. You're already paying interest on it. The idea behind debt recycling is to use that loan; specifically the equity you've already built up; to invest in income-producing assets like shares or ETFs.

Here's the cycle:

- You make extra repayments on your home loan

- You redraw that same amount through a separate investment loan

- You invest in income-producing assets; shares or ETFs that pay dividends

- The interest on the investment loan is now tax-deductible

- You repeat; pay down the home loan, redraw, invest

The end result: your home loan gets paid off, you build an investment portfolio, and the interest on your investment portion reduces your tax bill.

The ATO is clear on this. As their official guidance states: "If you borrow money to buy shares or other investments from which you earn dividends or other assessable income, you can claim a deduction for the interest you pay." Source: ATO — Interest, dividend and other investment income deductions.

The loan structure needs to be set up correctly; the investment and personal portions must be in separate splits to maintain the deductibility. This is a point worth getting right with a tax professional.

It’s about the returns stupid!

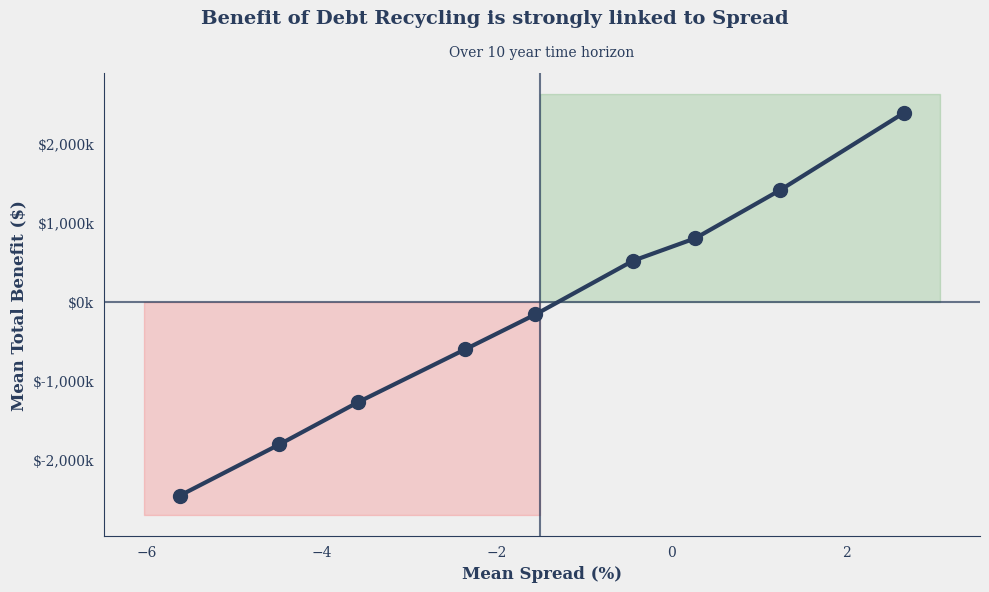

The best way to think about debt recycling is through one simple lens: the spread between your investment return (stock returns + dividends) and your interest rate.

Think of it as a chart with two zones:

Green zone - debt recycling works: When your stock growth exceeds your interest rate, the strategy generates positive net benefit that compounds over time. The wider the spread, the more powerful the strategy becomes. Over 10 or 15 years in the green zone, the wealth difference compared to not recycling can be very significant.

Red zone - debt recycling destroys wealth: When your stock growth is below your interest rate, you are paying more in interest than your investments are returning. The tax deduction reduces the damage but does not eliminate it. You are still going backwards. The further you are into the red zone, the faster you lose ground.

The key insight: the tax deduction shifts the breakeven point; it lowers the effective interest rate you're paying, making it easier to stay in the green zone. But it cannot move you from the red zone to the green zone on its own if your investment returns are genuinely poor.

This is why leading with tax benefits is misleading. The tax benefit is a tailwind when returns are not as strong. It offsets poor returns but is not a booster for strong returns.

What Do the Current Numbers Look Like?

Interest rate side:

The RBA cash rate is currently 4.35% following the May 2026 rate decision. Source: RBA — Cash Rate Target. Variable home loan rates for investors run above the cash rate — typically in the 6–7% range depending on the lender and loan type.

The RBA's CPI inflation rate as at April 2026 is 4.2%. Source: RBA. This matters because it affects the real cost of your debt and the real return on your investments.

Investment return side:

The long-term average annual return for Australian shares; including dividends reinvested; is approximately 10% per annum (to June 2025) based on RBA historical data covering Australian equities from the early 20th century to present. Source: RBA Research Discussion Paper 2019-04 — A History of Australian Equities.

This 10% is a long-run average. Individual years vary dramatically, the ASX has returned more than 20% in some years and fallen more than 30% in others. The strategy depends on the long-run average holding over your investment horizon, not on any individual year performing well.

The spread today:

At a 7% variable investment loan rate and a 10% long-term expected return, the gross spread is approximately 3%. After the tax deduction on interest (which effectively lowers your borrowing cost), the after-tax spread widens, but the margin is not wide. This is not the same environment as 2020 or 2021 when rates were at historic lows and the spread was much more favourable.

This matters for anyone considering starting debt recycling in 2026. The maths still works on long-run averages; but the margin for error is thinner than it was two years ago.

When Returns Aren't There: The Risk That Matters

Here is the scenario that most debt recycling articles don't spend enough time on.

Your investment portfolio falls 20% in a market downturn. Your loan balance does not fall. You are still paying interest every month on the full amount you borrowed. Your net wealth has declined; the value of your portfolio is now less than the debt against it.

The tax deduction continues. But it doesn't change the fact that you owe more than your portfolio is worth, which is the main driver of wealth creation in this strategy,

This is not a theoretical risk. The ASX fell approximately 37% during the COVID crash of early 2020. It fell approximately 7% in 2022 as interest rates rose sharply. Anyone who started debt recycling at the wrong point in the cycle faced exactly this situation.

Faithfully, markets do recover. The ASX has recovered from every major downturn in history. Investors who stayed the course during COVID recovered fully within months. Source: RBA Statistical Table F7 — Share Market.

But recovery assumes you don't sell. And not all recoveries are over the course of months, sometimes they take years to return. The risk of being forced to sell; because of income loss, rising rates, or a life event; is why the strategy requires stable income and financial stability.

What the Tax Deduction Actually Does

The tax deduction is confirmed by the ATO, and has been in place for decades. Source: ATO — Dividend income deductions.

What it does is lower your effective borrowing cost. If your investment loan rate is 6.5% and your marginal tax rate is 37%, the deduction reduces your after-tax cost of borrowing to approximately 4.1% (assuming no dividend income). This effectively widens your spread versus expected investment returns.

What it does not do is make a bad investment good. If your shares fall 20% in a year, the tax deduction on your interest does not offset a 20% capital loss. The deduction is worth something; it reduces the damage. But it cannot substitute for the returns that make the strategy work.

This is the honest framing that most articles miss. Tax benefits are secondary. Returns are primary.

Who Should Consider It, and Who Shouldn't

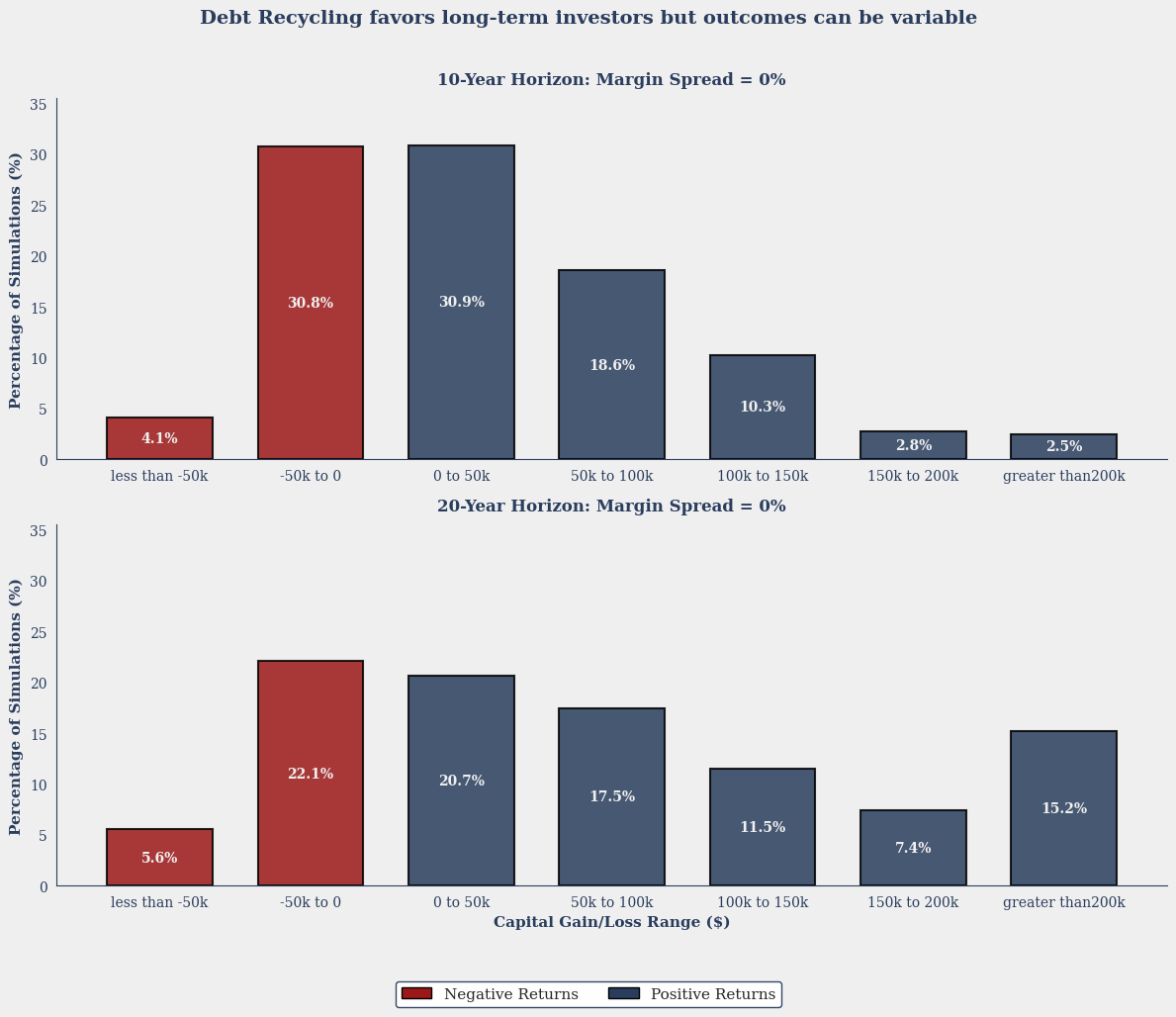

Not every investor is suited to debt cycling, and one variable that gets underestimated more than almost any other is time. How long you stay invested doesn't just affect outcomes at the margin; it can be the difference between the strategy working as intended and it working against you.

The impact of your investment horizon

A 10-year horizon and a 20-year horizon may appear similar, but the additional time can y influence the risk and return profile of the strategy. Over 10 years, investment outcomes are still relatively dependent on the sequence of returns experienced along the way. Over 20 years, there is more time for periods of weaker performance to be offset by subsequent growth, which can lead to a more favourable distribution of outcomes.

This is why 3-5 years may not be a sufficient time horizon for debt recycling. The client who commits to 10-20 years or more is not just hoping for more growth; they are materially improving the statistical probability of the strategy working in their favour.

The simulation data above shows the distribution of capital gain and loss outcomes across thousands of Monte Carlo scenarios; comparing a 10-year horizon against a 20-year horizon, both at a zero margin spread. The second graph shows less negative performance and stronger tailed positive returns.

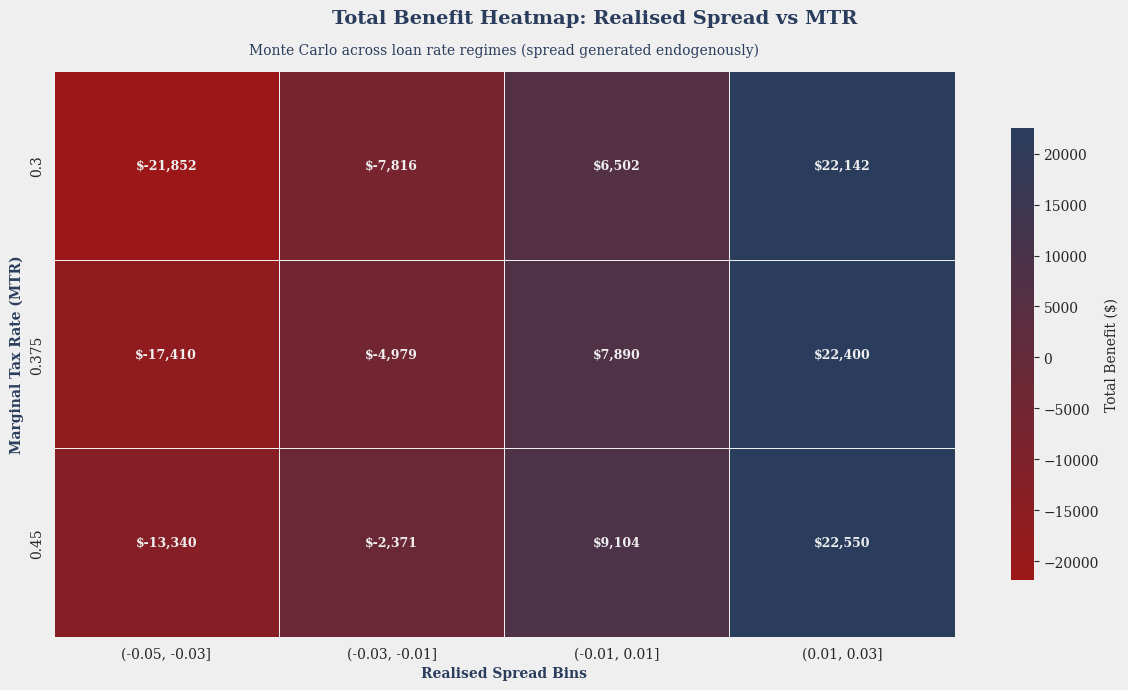

What the Data Shows: MTR vs Realised Spread

The heatmap below plots total benefit across different marginal tax rates (MTR) and realised spreads; the difference between your investment return and your interest rate.

The pattern is clear. When the spread is positive; when your investments are outperforming your borrowing costs; your marginal tax rate makes almost no difference to the outcome. All three tax brackets produce similar results in the $22,000+ range.

Where MTR begins to matter is when spreads turn negative. At a -5% to -3% spread, a 45% MTR produces a loss of $13,340 versus $21,852 at 30%. The tax deduction softens the blow at higher income levels; but it cannot prevent a loss when returns genuinely disappoint.

The takeaway: don't choose debt recycling because of your tax rate. Choose it; or don't; based on your view of long-term investment returns relative to your borrowing cost. The tax benefit is a modifier, not the foundation.

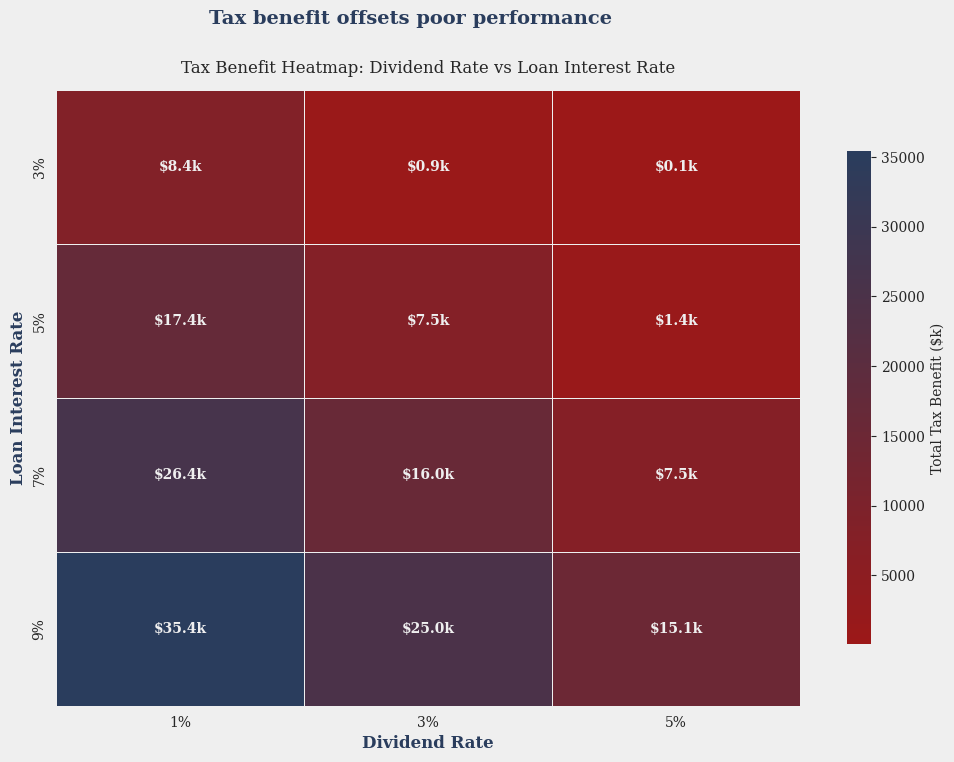

Tax Benefit Heatmap: Why Growth Stocks Work Better

This chart plots total tax benefit across different dividend rates and loan interest rates.

The highest tax benefit, $33.4k, occurs when the dividend rate is low (1%) and the loan interest rate is high (9%). The lowest tax benefit occurs when dividend rates are high and interest rates are low.

This produces a counterintuitive insight: to maximise the tax benefit of debt recycling, growth-focused investments; characteristically low dividend yield with higher capital appreciation; are more effective than high-yield dividend stocks.

The reason is straightforward. The tax deduction applies to your interest expense, not your dividend income. A higher interest rate means a larger deduction. And a lower dividend rate means less assessable income being generated; which keeps your taxable income lower while the deduction works in your favour.

This does not mean high-yield dividend stocks are wrong for debt recycling. But if maximising the tax efficiency of the strategy is a priority, growth-oriented investments deliver a structurally better outcome than income-heavy ones.

It makes sense for people who:

- Have a stable, high income and can service the debt even if markets fall or income drops temporarily

- Have significant home equity and a mortgage with a redraw or split facility

- Are investing with a genuine 10–20 year horizon and won't need to access the funds

- Understand that the strategy involves real risk of capital loss and are financially prepared for a downturn

- Have a registered tax agent who can structure and review the loan split annually for ATO compliance

It does not make sense for people who:

- Have variable or uncertain income

- Need liquidity; the investment portion should be considered locked for the duration

- Are close to retirement and cannot afford a significant portfolio drawdown

- Are doing it primarily for the tax saving without understanding the return dependency

The Honest Verdict

Debt recycling is a legitimate wealth-building strategy when it's a long term investment. The tax deduction is real. The long-run case for Australian shares generating returns above borrowing costs is supported by history, but the long term is not always what you will experience.

But the marketing around it oversells the tax angle and undersells the return dependency. The tax benefits mean nothing if your investments underperform your interest rate. The strategy lives and dies on that spread; and that spread is not guaranteed.

In 2026, with the RBA cash rate at 4.35% and variable investment loan rates running at 6–7%, the margin is thinner than it was in the low-rate environment of 2020–21. The strategy can still work over a long horizon. But it requires more patience, more resilience, and more financial cushion than the headlines suggest.

If you are serious about it, the next step is a conversation with a licensed financial adviser and registered tax agent who can model the numbers against your actual income, equity, and cash flow; not a generic illustration.

Already thinking about how this fits into your broader retirement picture? Delphi IQ can help you model your super projections and retirement income alongside other wealth strategies; free and built for Australia's super system.

This article is for general informational purposes only and does not constitute financial, tax, or legal advice. Seek advice from a licensed financial adviser and registered tax agent before implementing a debt recycling strategy.

FAQs

What is debt recycling in Australia?

Debt recycling is a strategy that converts non-deductible home loan debt into tax-deductible investment debt without increasing your total borrowing. You make extra repayments on your home loan, redraw that amount into a separate investment loan, and invest in income-producing assets. The interest on the investment loan is tax-deductible under ATO guidelines. Source: ATO — Interest, dividend and other investment income deductions.

Is debt recycling legal in Australia?

Yes. The ATO confirms that interest on money borrowed to buy income-producing shares or investments is tax-deductible. Source: ATO — Dividend income deductions. The loan must be structured correctly with investment and personal debt in separate splits.

When does debt recycling work?

It works when your investment return exceeds your after-tax interest rate. Based on long-run RBA data, Australian shares have returned approximately 8% per year on average including dividends. Source: RBA Research Discussion Paper 2019-04. With the RBA cash rate at 4.35% as at May 2026 and variable investment loan rates above that, the strategy works on long-run averages; but the spread is narrower than it was in the low-rate period of 2020–21.

Source: RBA — Cash Rate Target.

What are the risks?

The main risk is that your investment portfolio falls while your loan balance stays the same. You continue paying interest on a loan that is now larger than your portfolio's value. The tax deduction reduces the cost but does not eliminate the loss. The strategy requires genuine financial resilience; stable income, a long time horizon, and the ability to ride out a significant market downturn without being forced to sell.

Does the tax deduction make debt recycling worthwhile even in a bad year?

No. The tax deduction lowers your effective borrowing cost, which widens the spread between your investment return and your interest rate. But if your investments genuinely underperform your interest rate, the tax saving does not make up the difference. Returns are primary. The tax benefit is secondary.

Do I need a financial adviser to do debt recycling?

Yes. The loan structure must be set up correctly for ATO compliance; investment and personal debt cannot be mixed in the same account or the deductibility may be disallowed. You also need a registered tax agent to review the structure annually. Speak with a licensed financial adviser and registered tax agent before implementing.