How First Home Super Saver Scheme Actually Works?

.webp)

Is the First Home Super Saver Scheme Actually Worth It?

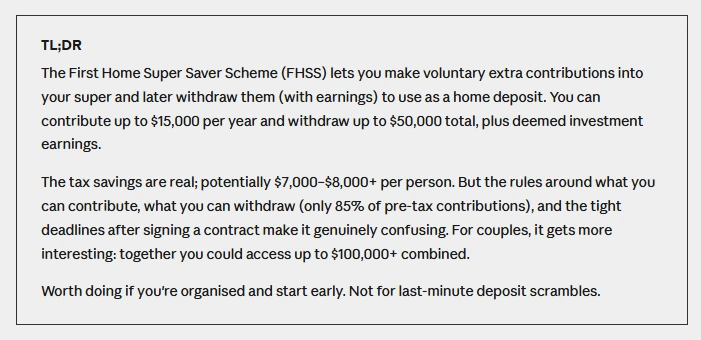

It’s harder than ever for first-home buyers in Australia, with sky-high property prices and deposits that feel unreachable. But what if there was a way you could grow your deposit faster? Enter: the First Home Super Saver Scheme (FHSS). This government initiative allows first-home buyers to withdraw eligible parts of their super fund as a tax-effective way to save up to $50,000 of their home deposit.

Don’t know what it is and how it works. Here's the honest breakdown.

What Is the FHSS Scheme?

The First Home Super Saver Scheme (FHSS) is an Australian Government initiative that lets first home buyers boost their deposit savings by making extra contributions into their superannuation fund, and then withdrawing those contributions (plus investment earnings) when they're ready to buy.

The idea is simple: super is taxed at a flat 15%, which is lower than most people's marginal income tax rate. So if you sacrifice $15,000 into super instead of taking it as income, you pay less tax on that money. When you withdraw it later for a home deposit, you've effectively saved the difference.

For the 2025–26 financial year, the annual contribution cap remains $15,000 and the total lifetime cap is $50,000. These limits sit inside your normal concessional contributions cap, which is $30,000 for 2025–26, so your employer's super guarantee contributions count toward that cap too.

The Part That Trips Everyone Up: Withdrawals

This is where the scheme gets messy; and where most people get caught off guard.

You cannot simply withdraw the full amount you put in. The ATO lets you withdraw 85% of eligible before-tax (concessional) contributiohttps://www.ato.gov.au/individuals-and-families/super-for-individuals-and-families/super/withdrawing-and-using-your-super/early-access-to-super/first-home-super-saver-schemens, and 100% of after-tax (non-concessional) contributions. So if you contribute the full $50,000 in pre-tax dollars, you'd get $42,500 back, not $50,000.

Note: On top of that 85%, you also receive deemed investment earnings; a growth rate applied by the ATO (currently around 7.17% to 7.42% per quarter, based on their shortfall interest charge). This means your actual withdrawal could be higher than $42,500, but you won't know the exact figure until you apply for a determination from the ATO.

You can't easily budget around a fixed number. Your withdrawal depends on how you contributed, when you contributed, and the ATO's deemed earnings rate at the time of release. There's also a critical rule about timing. You must notify the ATO within 90 days of signing a contract to purchase or build your home, or an extra tax of 20% may apply. This is a deadline that catches a lot of buyers by surprise.

Your Boss's Super Does Not Count

This is the number one misconception. You cannot use your employer's compulsory Super Guarantee contributions under this scheme. Only eligible voluntary contributions you choose to make yourself are releasable under the FHSS scheme; salary sacrifice amounts, personal deductible contributions, or after-tax contributions you make yourself.

What's excluded:

- Compulsory employer Super Guarantee contributions

- Spouse contributions made on your behalf

- Government co-contributions

- Downsizer contributions or contribution splitting amounts

If you've been assuming your employer's super is quietly building your deposit fund, it isn't.

The Tax Saving: Is It Real?

Yes; but the numbers require context. Based on average full-time earnings of around $101,670 per year, salary sacrificing $10,000 a year into the scheme could produce around 7.9% more savings after one year versus a standard savings account, rising to around 11.5% after five years.

For most people on average incomes or above, the real-world savings per person lands around $7,000–$8,000 on a full contribution over a few years. For couples, that doubles; which is where the scheme starts looking genuinely compelling.

Who benefits most:

- Higher earners (higher marginal tax rate = bigger gap vs. 15% super tax)

- Couples buying together up to $100,000+ (it's $50,000 per person)combined release

- People with 2–5 years before they plan to buy

- Those who already salary sacrifice or make personal deductible contributions

Who Is Eligible?

The basic eligibility rules are:

- You have not previously owned property in Australia (with a hardship exception)

- You intend to live in the property for at least 6 months within the first 12 months after it can be occupied

- You have not previously made an FHSS release request

- The property must be residential premises in Australia (vacant land only if you plan to build)

The ATO checks your eligibility both when you apply for a determination and again when you request your release; so don't assume you're in the clear after the first step.

How to Actually Use It — Step by Step

1. Check your eligibility: The basic requirements: you haven't previously owned property in Australia (there's a financial hardship exception), you intend to live in the property for at least 6 months within the first year, and you've never made an FHSS release request before. Check the full criteria at the ATO's FHSS page.

2. Start making voluntary contributions: Set up salary sacrifice through your employer, or make personal after-tax contributions to your super fund. Only contributions made from 1 July 2017 onward are eligible.

3. Request a determination from the ATO: Log into myGov, link it to the ATO, and request an FHSS determination. This tells you exactly how much you're eligible to release. It's non-binding, free, and worth doing periodically.

4. Request your release when you're ready:The ATO instructs your super fund to release the funds, withholds applicable tax, and sends the remainder to you. It can take up to 25 business days to receive your funds after a valid request. AustralianSuper

5. Notify the ATO within 90 days of signing: After signing a contract to buy or build, you must notify the ATO within 90 days. Miss this deadline and you could face a 20% tax hit.

The Verdict

If you're buying in the next 2–5 years and you're disciplined about making voluntary contributions, the FHSS scheme is genuinely worth doing. The tax savings are real. The confusion is also real, but it's navigable with a bit of planning upfront.

It's not a magic shortcut. It's a patient, structured tool that rewards people who start early. If you're six months away from buying and haven't contributed yet, it won't move the needle much. But if you start now, it will.

For the most up-to-date rules and contribution caps, always refer directly to the ATO's official FHSS guide or speak to a licensed financial adviser before making contribution or withdrawal decisions.

Already own your home and thinking about what comes next? If you're building toward retirement, Delphi IQ can help you model your super projections and retirement income; for free.

This article is for general informational purposes only and does not constitute financial, tax, or legal advice.